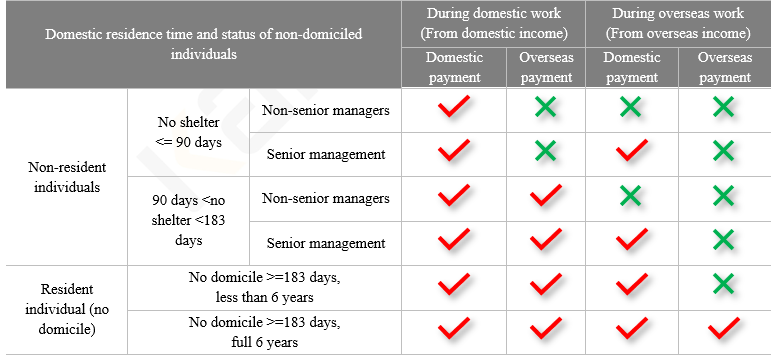

Q:

|

What is the difference between an individual without a domicile and an individual without a domicile in the calculation of wages and salaries?

|

A:

|

|

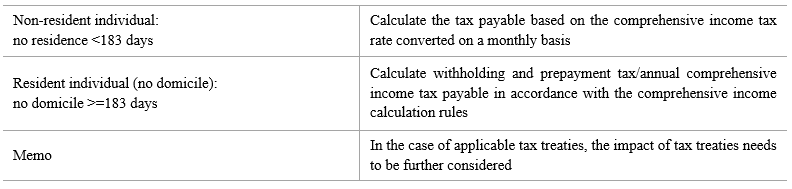

Q:

|

Combined with the current comprehensive income tax calculation method under the new personal income tax law, how to calculate the personal income tax of non-resident individuals or non-resident individuals without domicile?

|

A:

|

|

Q:

|

Regarding the time judgment of resident individuals, how is the tax treaty different from China's personal income tax law?

|

A:

|

-

The 183 days in the Chinese tax law means that the accumulative stay in China is less than 183 days in a tax year;

-

The 183-day rule in the tax treaty: Stay in the other party for a continuous or cumulative period of no more than 183 days during any twelve months at the beginning or end of the relevant tax year.

|

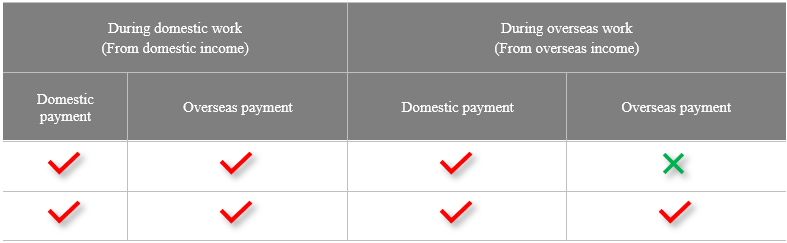

Q:

|

If the individual is a senior manager and the agreed director’s fee clause applies, how to calculate?

|

A:

|

When the individual is a senior-manager and applied the agreed director fee clause, as the following:

|

Q:

|

If the tax treaty and the individual income tax law are different in calculating personal income, which one should be applied?

|

A:

|

Here, the principle of "advanced excellence" applies. That is, if the tax burden stipulated in the tax treaty is more favorable than the individual income tax law, the taxpayer can apply for tax treaty treatment, and vice versa. Therefore, how taxpayers ultimately calculate their taxes requires comprehensive consideration of various regulations such as the Individual Income Tax Law, tax treaties and individual income tax preferential policies.

|