Q:

|

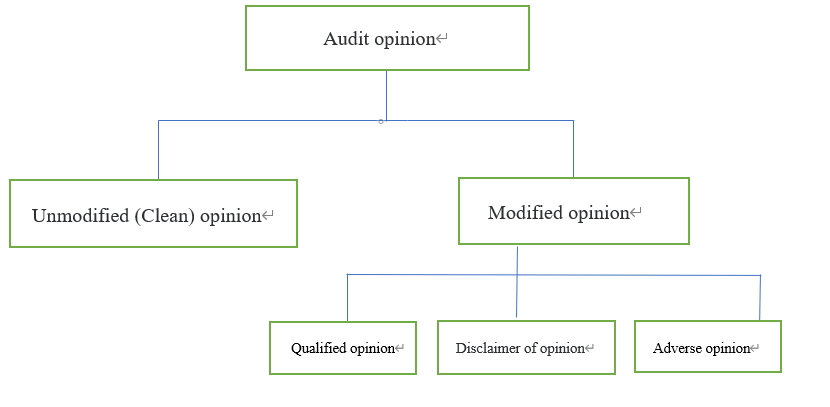

How many different types of audit opinions in audit report?

|

A:

|

There are two main types of audit opinions: unmodified (clean) opinion and modified opinion. Thereinto, modified opinions are divided into three types, which are qualified opinion, disclaimer of opinion and adverse opinion. Please see the following flowchart:

|

Q:

|

When will an unmodified (clean) opinion be given?

|

A:

|

In accordance with the Hong Kong Auditing Standards, the audit evidences obtained by the auditors are sufficient and appropriate to provide a basis for the audit opinion, and thus, an unmodified audit report can be given. Generally, an unmodified opinion is given because no noteworthy violations or major errors were found in the company's financial report.

|

Q:

|

When will a qualified opinion be given?

|

A:

|

According to the Hong Kong Auditing Standards and the Hong Kong Companies Ordinance, the auditor is unable to obtain sufficient audit evidences during the audit, in other words, if material misstatements are found in the financial statements during the audit, the auditor will give an qualified opinion in the report.

|

Q:

|

When will a disclaimer of opinion be given?

|

A:

|

Disclaimer of opinion is more serious than a qualified opinion. If sufficient audit evidence cannot be obtained and prove the amount stated on the financial statement, disclaimer of opinion will be given. According to Article 405 of the Hong Kong Companies Ordinance, auditors are not responsible for the content of audit reports.

|

Q:

|

When will an adverse opinion be given?

|

A:

|

Adverse opinion is generally given because the financial statements violate Hong Kong accounting standards and the Hong Kong Companies Ordinance, and the information provided is inaccurate and unreliable. As with being the disclaimer of opinion, according to section 405 of the Hong Kong Companies Ordinance, auditors are not responsible for the content of the audit report.

|