|

Q:

|

What kind of conditions should be satisfied

before a deduction for home loan interest is granted in Hong Kong?

|

|

A:

|

All of the following conditions must be satisfied before a

deduction for home loan interest paid is granted:

|

|

Q:

|

What is the tax treatment if I own more than one

place of residence in Hong Kong?

|

|

A:

|

You are entitled to claim the deduction for your principal

place of residence only if you own more than one place of residence.

-

you are the registered owner of the dwelling/property, either as a sole

owner, a joint tenant or a tenant in common, as shown in the records of the

Land Registry;

-

the dwelling is a separate rateable unit under the Rating Ordinance, i.e.,

it is situated in Hong Kong;

-

the dwelling is used wholly or partly as your place of residence in the year

of assessment (interest deductible will be prorated if the dwelling is partly

used as place of residence);

-

the home loan interest paid during the relevant year

of assessment was for a loan for acquisition of the dwelling;

-

the loan is secured by a mortgage or charge over the dwelling or over any

other property in Hong Kong; and

-

the lender is an organization prescribed under section 26E(9) of the Inland

Revenue Ordinance.

|

|

Q:

|

What is the maximum number of years of

deduction?

|

|

A:

|

The number of years of deduction for home loan interest is extended from

10 to 15 years of assessment effective from the year of assessment 2012/13,

while it was further extended to 20 years starting from the year of assessment

2017/18. Claiming for deduction for home loan interest in consecutive years is

not necessary. The current deduction ceiling is HK$100,000 for a year.

|

|

Q:

|

If my income from employment is less than personal

allowances, what is the tax treatment on the interest paid during the relevant

year of assessment?

|

|

A:

|

Since your income is less than your personal

allowances, you are exempt from tax even without taking into account the

deduction of home loan interest. In this situation, you will not be treated as having

been allowed the home loan interest deduction for that year and your remaining

years of entitlement for the deduction will be unchanged.

|

|

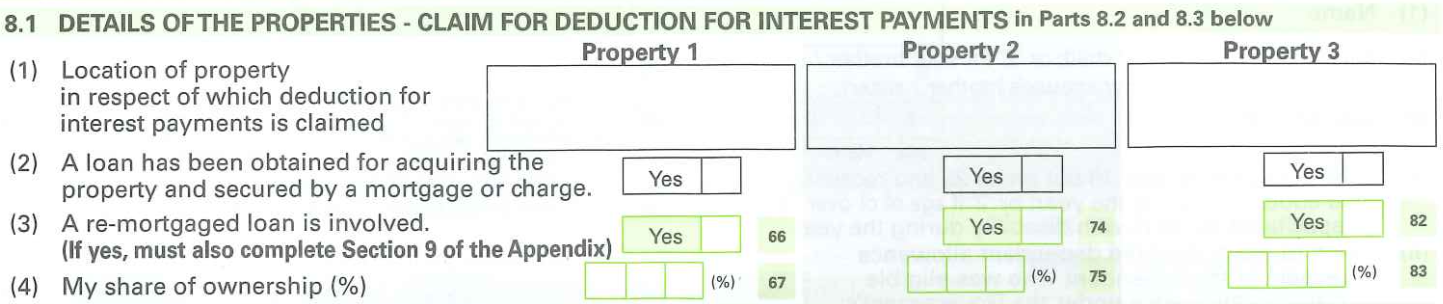

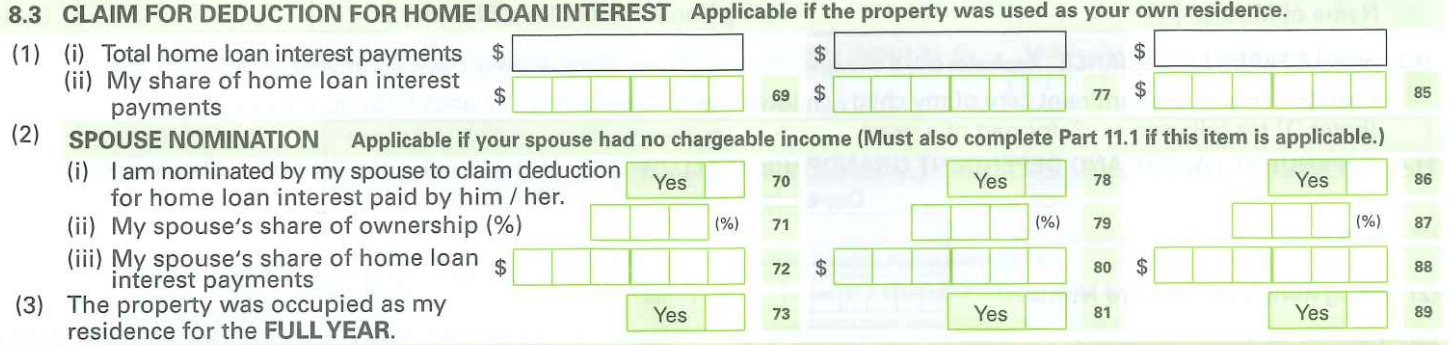

Q:

|

How can I claim the deduction for home loan

interest in Hong Kong?

|

|

A:

|

You can claim a deduction for home loan interest

by completing Part 8.1 and 8.3 of your tax return (BIR60) for the relevant year

of assessment.

|