![]() Laman Utama

Laman Utama

![]() Pengetahuan

Pengetahuan

![]() Amerika Syarikat

Amerika Syarikat ![]() Percukaian Amerika Syarikat

Percukaian Amerika Syarikat ![]() U.S. Tangible Property Regular MACRS Depreciation

U.S. Tangible Property Regular MACRS Depreciation

|

(1) |

Categorize any recently acquired depreciable assets that have been put into use during the fiscal year according to their respective MACRS classes; |

|

(2) |

Determine MACRS conventions; |

|

(3) |

Calculate "regular" MACRS depreciation (both first-year assets and assets placed in service in prior periods). |

|

|

(1) |

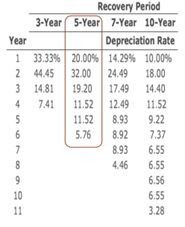

Half-year (HY) The cost of property in the 3-, 5-, 7-, and 10-year classes is recovered using the 200-percent declining-balance method, switching to the straight-line method in the year when that maximizes the deduction (IRC Section 168(b)(1)). HY is general rule: The general rule is that all assets are placed in service at the half-year regardless of when they were actually placed in service. Thus, for a calendar-year taxpayer, all assets are treated as placed in service on 7/1. |

|

(2) |

Mid-quarter (MQ) The cost of 15- year and 20-year property is recovered using the 150% declining balance method, switching to the straight-line method to maximize the deduction (IRC Section 168(b)(2)). MQ is exception: If more than 40% of assets by value subject to HY/MQ were placed in service in 4Q (10/1–12/31 for calendar year taxpayers), the MQ convention applies (not HY). |

|

(3) |

Mid-month (MM) The cost of 27.5- year (residential) and 39-year (non-residential) real property is recovered using the straight-line method. Assets are treated as placed in service in the middle of the month in which they were actually placed in service. |

|

Penafian

Segala maklumat dalam artikel ini adalah untuk tujuan perkongsian maklumat sahaja dan bukan merupakan nasihat profesional. Kaizen tidak akan bertanggungjawab terhadap sebarang kerugian atau kerosakan yang timbul daripada penggunaan maklumat tersebut.

|

Bahasa

Tutup